IS P2P RIGHT FOR ME?

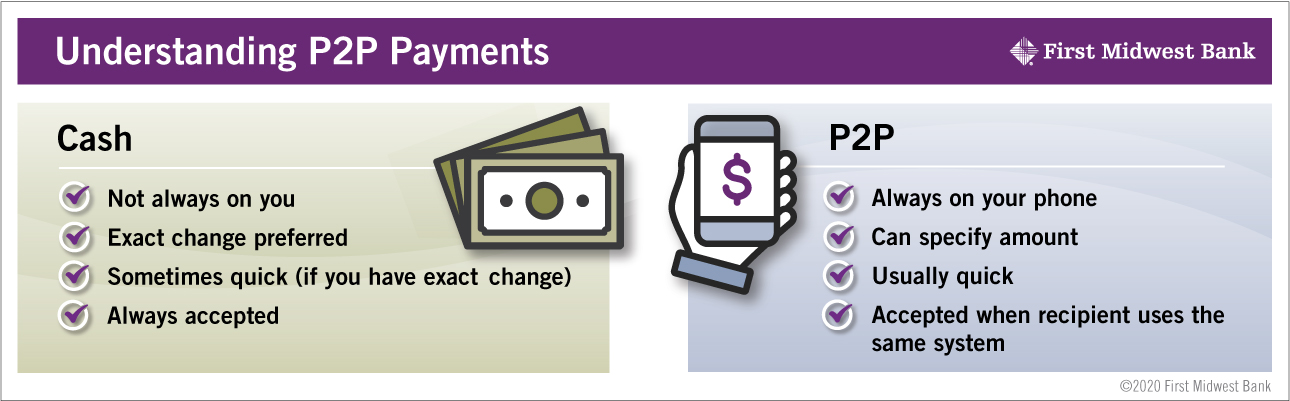

What is a peer-to-peer (P2P) payment? Think of it as a digital replacement for cash or a check. Rather than using physical dollar bills to pay your friends and family, you can use an app on your phone. Depending on the platform you use, your money may be received within minutes of when you hit send.1

Peer-to-peer payments offer the benefit of convenience and, in many cases, speed. For example, say you are at a coffee shop before a concert. Your friend bought the concert tickets and you bought the coffee. But, the tickets cost five times as much. How do you even up?

Rather than finding an ATM, or asking a barista to break a large bill, or mailing a check when you get home, you can send the exact amount with a few clicks on your phone. And that’s it; you did it without even leaving your seat.

How Do I Set Up Peer-to-Peer Payments?

Peer-to-peer payments may be easier to activate than you think. Many banks and credit unions support a P2P system within their own apps, for example, by offering access to Zelle®. Check with your financial institution to see if Zelle or another P2P solution is offered. By using the P2P app offered by your financial institution, you will likely benefit from an easy set-up.

Or, if you have accounts with Apple™ or Google™, you can link a credit or debit card to your account and use Apple Pay™ Cash and Google Pay™, respectively. Lastly, if none of the above options make sense, you can download another P2P app of your choice and link it to a credit card, debit card, or bank account.

What is the Best Peer-to-Peer Payment App to Use?

While the user experience is important, remember that many apps can only transfer payments to individuals who also use the same app. For example, even if you really like the interface of a lesser-known P2P app that functions in this manner, if none of your friends are on it, it doesn’t help you much.

Keep in mind, though, that Zelle is already available to over 140 million consumers in their mobile banking app or through the Zelle app. So even if your friends don't use the same bank as you, you can still send and receive money quickly and easily with almost anyone who has a U.S.-based bank account. As of this writing, Zelle is offered by 827 different financial institutions, including First Midwest Bank. See if your bank is included.

If your bank doesn’t use Zelle, PopMoney is another app that connects through many banking apps. Or, Venmo is a popular stand-alone app.